Commercial mortgages are a financing option for businesses looking to purchase property for their operations. Unlike residential mortgages, a commercial mortgage can be more complex and have different requirements and terms. To apply for a commercial mortgage, businesses must provide financial statements, tax returns, and proof of income, among other documents.

Advantages of Purchasing Commercial Real Estate

One advantage of buying commercial property with a mortgage is that it gives businesses an opportunity to build equity in the property. Owning a property can also offer more stability and control over the space, allowing businesses to make modifications or improvements without seeking permission from a landlord.

However, commercial mortgages also come with risks and costs. For one, the loan amount may come with high interest rates, making the financing option less attractive than leasing. Additionally, businesses need to consider the expenses involved in maintaining and managing the property, such as property taxes, insurance, and repairs.

Getting a Commercial Mortgage in Ontario Involves Several Steps.

First, you need to have a solid business plan and financial statements to present to potential lenders. You will then need to shop around for a lender that offers specialized commercial mortgages to businesses in your industry, size, and creditworthiness. The lender will evaluate your application based on a variety of factors, including the stability of your business, your credit history, your income, and the value of the property.

Typically, lenders require a down payment of 20% or more, and the interest rates for commercial mortgages can vary widely depending on the lender, your credit score, and the type of loan you select. In Ontario, the current average interest rate for commercial mortgages is around 5%. To qualify, you will need to demonstrate your ability to repay the loan and provide evidence that you have an established business with a steady income stream.

Leasing vs. Purchasing Commercial Property

Leasing, on the other hand, may be more flexible and affordable, allowing businesses to relocate or upgrade their space without the long-term commitment of a mortgage. It also provides a predictable monthly cost, which can help with budgeting and financial planning.

In conclusion, both buying and leasing commercial property come with their own set of pros and cons. It’s important for businesses to carefully consider their options and weigh the risks and benefits before making a decision. Ultimately, the choice should be based on the business’s current financial situation, long-term goals, and overall needs.

You should have a clear reason for mortgage refinance – whether that’s to shorten the term of the loan, reduce your monthly payment, or even pull equity out of the property for the purpose of debt repayment or home repairs.

II. Check Your Credit History and Score

You will have to qualify for the refinance just as you needed to for approval of the original home loan. The higher the credit score, the better the refinance rates you are likely to be offered by lenders and the higher the chances of your loan being approved.

While there are several different ways to refinance your mortgage even if you have bad credit, take a few months to boost your credit score, if possible, before getting started with the process.

III. Determine the Amount of Equity You Have in Your Home

The equity in your home refers to the total value of the property minus what’s owed on your mortgage. You may be able to refinance a conventional loan with as little as 5% equity, but you will probably get better rates and fewer fees and will not be required to pay for PMI (private mortgage insurance) if you have at least 20% equity.

IV. Shop Multiple Lenders

You can literally save thousands if you get quotes from at least 3 mortgage lenders. The refinance rate table provided by Bankrate lets you comparison-shop loans, to ensure that you find the best fit for your financial needs.

V. Get Your Paperwork in Order

Gather recent federal tax returns, pay stubs, brokerage/bank statements, and anything else requested by your mortgage lender. Your lender will also consider your net worth and credit, so disclose all liabilities and assets upfront. If you have your documents ready before you get started with the process of refinancing, it will go on more smoothly and often faster.

VI. Prepare for Your Home to be Appraised

Mortgage lenders usually require a home appraisal, just like the one done when purchasing the property, to determine the current market value.

VII. Come to the Closing with Cash If Necessary

The closing disclosure and the loan estimate will likely list the additional expense in closing costs to finalize the loan. You might be required to pay 3% to 5% of the total loan at closing.

VIII. Keep Tabs on the Loan

Store copies of the closing paperwork in a safe location and automate the payments to ensure that you always stay current on the mortgage.

Why Compare 15-Year Mortgage Refinance Rates?

Shopping around for quotes from different lenders is an important step for every mortgage applicant. When shopping around, don’t just consider the mortgage rates being quoted but also the rest of the terms of the loan.

Don’t forget to compare APRs that include many extra costs of the mortgage not shown in the interest rate. Some lenders will have lower closing fees and costs than others, or your current credit union or bank may extend you a special offer.

Don’t also be afraid to walk away from your current lender when refinancing. If you’re able to find a better deal elsewhere, go for it. Consider quotes from traditional brick-and-mortar banks and online lenders. Alternatively, consider using a mortgage broker that provides quotes from wholesale lenders.

What Are the Pros and Cons of a 15-Year Mortgage Refinance?

Borrowers looking to retire their debt quickly usually find the shorter term of a 15-year loan appealing, but it does come with higher monthly payments. A breakdown:

Pros of a 15-Year Mortgage Refinance

You will fully own the property sooner. Compared to a 30-year loan, you will pay down the balance much faster.

You will save a lot on interest. Rates on 15-year loans are considerably lower than the rates on 30-year loans. Furthermore, you will pay less in interest over the life of the loan.

A larger portion of the monthly payments will go towards the principal on the loan rather than interest. With a 30-year mortgage, however, just a fraction of early payments goes towards retiring principal. A 15-year loan helps speed up the process.

Cons of a 15-Year Mortgage Refinance

Higher payments each month compared to longer-term loans because of the shorter period of repayment. If you are currently struggling to make the monthly payments, a 15-year mortgage will only make it more challenging.

The opportunity cost of having your money tied up in home equity as opposed to other financial assets. Perhaps it makes more sense to borrow more against your house and invest the proceeds for retirement.

The possibility of losing mortgage interest because of paying less in interest. The vast majority of Americans can no longer benefit from mortgage interest deductions, but if you currently do, you should consider the tax implications.

Not sure whether you should commit to higher monthly payments? It’s possible to mimic the effect of refinancing to a 15-year loan by making additional payments on your existing 30-year loan. You will shorten the pay-off time and pay less interest while still keeping some wiggle room.

If a financial emergency ever arises, you have the option to go back to the original, lower payment for that month, or for as long as you may need to. Best of all, you can do all that without incurring any penalties.

When Should I Consider a 15-Year Refinance?

If you currently have a 30-year mortgage, but have the budget for a higher mortgage payment each month, it can make good financial sense to refinance to a 15-year fixed-rate loan. You will still have the stability of knowing that your monthly payment will not change, while enjoying the benefit of a lower interest rate.

Furthermore, you will pay off the mortgage sooner, freeing up funds for other financial goals such as saving for retirement when you do. Keep in mind, however, that you will be required to prove to the lender that your income is sufficient to cover a higher payment so that you can qualify for the new loan.

If your goal is achieving the lowest payment possible, however, you are better off refinancing to a 20- or 30-year mortgage. Starting fresh with a new long-term loan might not necessarily be the best strategy for everybody, but it’s still an option, especially if you’re looking to trim monthly expenses.

Best Year Mortgages offers mortgage refinance services tailored uniquely to you. To learn more, contact us.

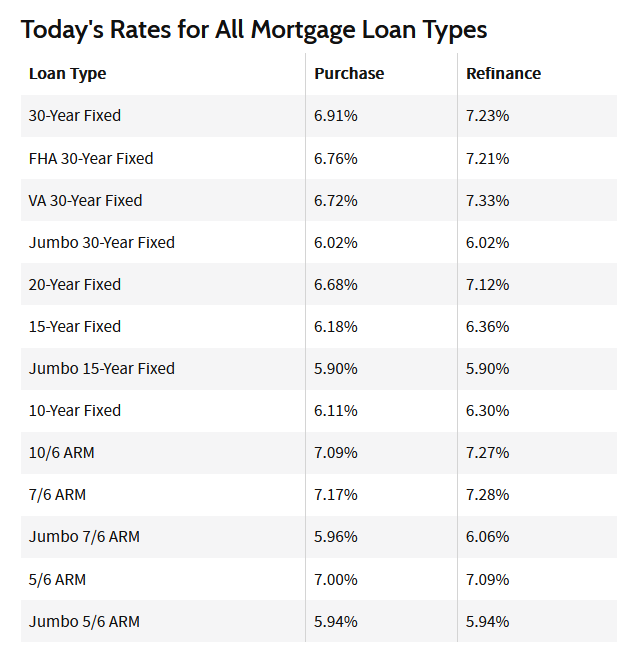

The current fixed 15-year mortgage rate across the US stands at 6.18%, while the jumbo 15-year mortgage rate is 5.90% since April 24, 2023. These specific mortgage rates are definitively not the enticing, temporary rates that lenders use in advertisements, but rather a reflection of what borrowers can reasonably expect to secure with their personal qualifications.

The standard 30-year mortgage is not the only option available to homeowners. People who qualify for a 15-year mortgage and secure the best rates could potentially save thousands in interest payments. Despite having a larger monthly payment, people who are financially prepared can benefit from lower interest rates. They may also build equity on their home at a quicker rate.

There’s importance in making an informed decision on whether a 15-year mortgage is right for you. It’s crucial to ensure that finances are strong enough to handle the higher payments that come with a shorter-term loan.

Should You Consider a 15-Year Mortgage?

If you can afford to make higher monthly mortgage payments and are looking to save significantly on your home loan, 15-year mortgages may be best for you.

These loans typically come with low interest rates, as agencies supported by the government often apply loan-level cost accommodation that can ramp up the cost of thirty year mortgages.

However, borrowers should carefully decide if they could pay higher monthly payments which are associated with 15-year mortgages compared to the lower payments of both 20 and 30 year long mortgages.

15-Year Mortgages Rates

Mortgage rates are determined by several factors. For example, a credit score, down payment amount, and the current market conditions. The best interest rate you can get may be higher or lower than your areas typical rate, depending on your financial profile.

So, if the prevailing rate is, let’s say 7%, your creditworthiness and other financial factors could lead to being offered a rate of 7.3% or 6.75%.

30-year rates are higher than 15-year rates

Mortgage rates are influenced by the prices of bonds funded securities market for mortgages. Bond investors are interested in low-risk investments with decent returns that maintain inflation rates.

Risks and inflation rates tend to increase with time. Long term loans have bigger interest rates than the shorter-termed ones. It’s challenging for investors to forecast risks and inflation rates far into the future.

Government-supported agencies also impose extra charges on higher loan levels. This causes the cost of thirty year long mortgages to rise. Lots of mortgages with a 15 year term do not have these additional charges, resulting in a decreased interest rate.

What Is a 15-Year Mortgage?

In simple terms, the mortgage is a type of loan designed to finance a home investment. This loan has a fixed interest rate. The payment which is paid monthly, consisting of interest and principal, stays constant throughout the duration of the mortgage.

Unlike a traditional 30-year mortgage, a 15-year mortgage takes half of the time to pay off, thanks to its higher monthly payments. A shortened loan term, coupled with the high monthly payments, leads to significant savings.

Do the Feds Influence Mortgage Rates?

The Federal Reserve’s actions have an impact on mortgage rates. Except they don’t determine them outright. The Fed sets rates for lending federally that banks must pay to borrow from the government for short-term periods.

It is then more costly for Finance institutes to borrow from others, when inter bank rates rise, As a result, they modify their mortgage and loan rates, so they can account for the additional expenses.

It’s worth noting, there are more factors that influence the exact rate that a home buyer is offered, including their credit score, assets, and liability.

15-Year mortgage vs 30-Year

The primary difference between a 30-year and a 15-year mortgage is the repayment period. The mortgage for 30 years requires 360 monthly payments (roughly 30 years), while a 15-year mortgage requires less time.

Although the monthly payments for 30 years are lower because they are spread out among a longer time span, the borrower pays more interest over the years. This is because the borrower is double the payment time compared with a 15-year mortgage. Additionally, a larger interest rate may be charged for a 30-year mortgage.

When should you choose a 15 year long mortgage?

Opting for the 15 year mortgage term is a wise decision for those who wish to reduce their interest expenses while still being able to make bigger payments monthly without jeopardizing their other priorities.

However, it’s important to note that this may not be the best option for everyone. A borrower may not be able to afford the larger monthly payments. If they can’t pay without sacrificing contributions to their savings and retirement accounts, then a mortgage that’s long term may be more suitable.

For those with inconsistent income, this mortgage is only recommended if you have a practical strategy in place to continue making mortgage payments even during tight periods.

If you obtain a mortgage, having a plan in place can result in significant savings

The savings come with a payment that is higher monthly. It’s recommended to shop around for the best rates. Compare terms to ensure your mortgage is affordable and you can comfortably pay for it.

Conclusion

Remember that mortgage rates are subject to daily changes and this information is provided for informational purposes only. An individual’s income and credit profile are the main factors that determine the loan rates and terms they are eligible for. The loan rates do not encompass taxes or insurance premiums, and each lender has their own specific terms and conditions.

A mortgage can be defined as a type of loan specifically designed for purchasing or maintaining a property (land, a home, or any other type of real estate). While you apply for a mortgage, the borrower agrees to pay off the lender over time. This is often accomplished through a series of regular payments divided into principal payments and interest. However, the property will serve as collateral.

Because there are many mortgage lenders, a borrower has the right to choose their preferred lender. On the other hand, different borrowers have different requirements, including a minimum credit score, a down payment, and more. Of course, there is a thorough process before receiving a mortgage.

It is critical to note that mortgage types differ based on the needs of the borrower, like fixed-rate loans, conventional loans, and others.

How Does A Mortgage Work?

Mortgages allow you to purchase property or real estate without paying the full amount for it. What does this mean? It simply means that you, as the borrower, will have to pay for the loan plus interest for a specific number of years. This is until the property becomes yours. Traditional mortgages are mostly fully amortized. You’ll pay the same amount (principal and interest) until the loan’s paid off. Remember, typical mortgage refinancing terms range from 15 years to 30 years, with most preferring 30 years due to its low scheduled repayment plan.

If, for any reason, the borrower fails to pay the mortgage, the lender can foreclose on the property. That is because the mortgage is a lien against the property.

When residential home buyers take out mortgages, they pledge their house to lenders, which they can claim if they don’t pay. When the lender forecloses on the property, they can evict the borrower or residents. They can sell the real estate, and use the money from the sale to pay the mortgage debt.

What Is The Mortgage Process?

Anyone seeking to borrow a loan will apply to different mortgage lenders. All lenders will request proof that the borrower can repay the mortgage loan. As such, the lender will be required to provide recent tax returns, investment and bank statements, and proof of current employment. After this, the lender will check your credit.

If everything checks out, the application will be approved. However, the lender will offer a loan of a certain amount (all based on the information you provided). The borrower can apply for a mortgage after identifying the property they wish to purchase. This is a process known as pre-approval. Whenever a home buyer is pre-approved for a loan, it gives them an edge in the current housing market.

The moment the home buyer and seller agree on the terms of the home purchase and meet at closing, the borrower will make a down payment to the lender. The home seller will transfer ownership of the property to the buyer and receive the agreed sum. After this, the buyer will sign any mortgage documents. Some lenders may charge fees for originating the loan.

What Are The Types of Mortgages?

Mortgages are available in different types. Mortgages are most common in 15- and 30-year fixed rates. Some mortgage types are short-term (five years), while others are longer (up to 40 or 50 years). Of course, stretching the payment over a long period of time decreases the monthly payment, but increases the amount of interest to be paid.

Types of mortgages

Adjustable-rate Mortgage (ARM)

With this type of mortgage, the interest rate is fixed for an initial term. After the initial term, changes can be applied based on prevailing interest rates. The introductory rate is often below the market rate. This makes the mortgage affordable if the repayment period is short-term and expensive if the interest rate increases substantially.

Fixed-Rate Mortgage

This is the most common type of mortgage available to many. The benefit of this type of loan is that the interest rate stays the same until the completion of the loan repayment. It is also known as a traditional mortgage.

Interest-Only Loans

Although not very common, this type of mortgage can improve complex repayment schedules, and sophisticated borrowers should use it. Although the limitations of these loans may come with highly ballooned payments at the end, A majority of homeowners get into financial trouble because of this type of loan.

Reverse Mortgages

Just as the name suggests, these mortgages are very different financial products. That is because they are designed for homeowners aged 60 and above who wish to convert part of their equity into home cash. In this case, the homeowner can borrow against the value of their home. They can receive a lump sum amount, a fixed monthly payment, or a line of credit. The whole loan balance becomes due whenever the borrower dies, sells, or relocates permanently.

What Reasons Do People Need Mortgages?

One of the reasons people need mortgages is that the value or price of homes is far superior to the amount of money households can save. For this reason, many families prefer purchasing a home by putting down a relatively small amount, like 20%. They gain the rest through a loan.

What Is The Difference Between Fixed And Variable Mortgages?

Many mortgage types carry fixed or variable interest rates. With a fixed interest rate, the amount payable every month will not change until the mortgage is paid off. On the other hand, with a variable mortgage, interest rates rise and fall based on an agreed-upon percentage or interest rate variation.

Can I Mortgage Multiple Houses?

Lenders will have to first issue the first (principal) mortgage before they can grant a second one. The second loan is a home equity loan. Lenders do not provide an additional mortgage backed by the same property as the primary loan. Nevertheless, there are limits to junior loans on your property. The bottom line is that as long as you have equity, excellent credit score, and a low debt-to-income ratio, you can be approved for home equity loans.

Summary

It is clear that mortgages have become an integral part of our lives. It is the only option for many home buyers who do not have thousands of dollars to purchase a home without a loan. You just need to know that different types of mortgages have different benefits and limitations.